GENEVA, 5 February 2021: Airlines suffered the worst traffic decline in aviation history during 2020 and forward bookings suggest the first quarter of 2021 might not bring a marked improvement.

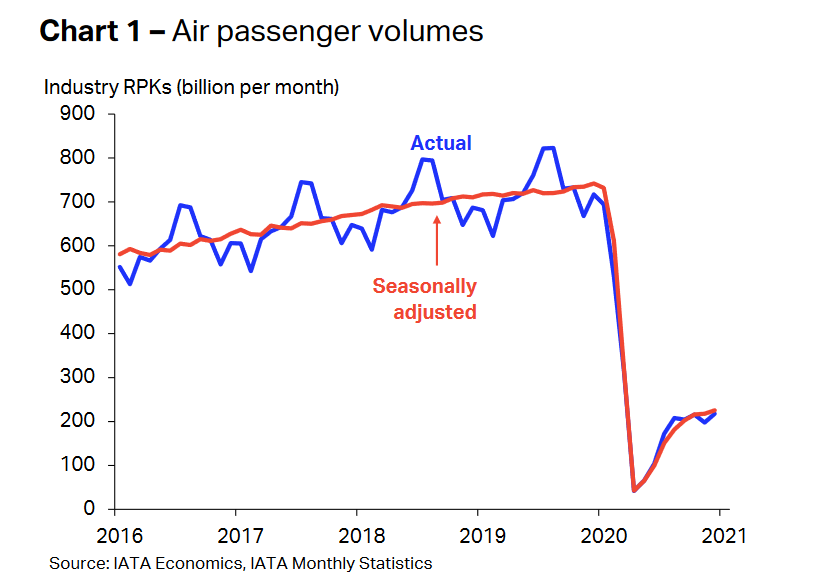

Earlier this week the International Air Transport Association (IATA) announced full-year global passenger traffic results for 2020 showing that demand (revenue passenger kilometres or RPKs) fell by 65.9% compared to the full year of 2019 by far the sharpest traffic decline in aviation history. The outlook remains grim for Q1 2021 as advance bookings have been falling sharply since late December.

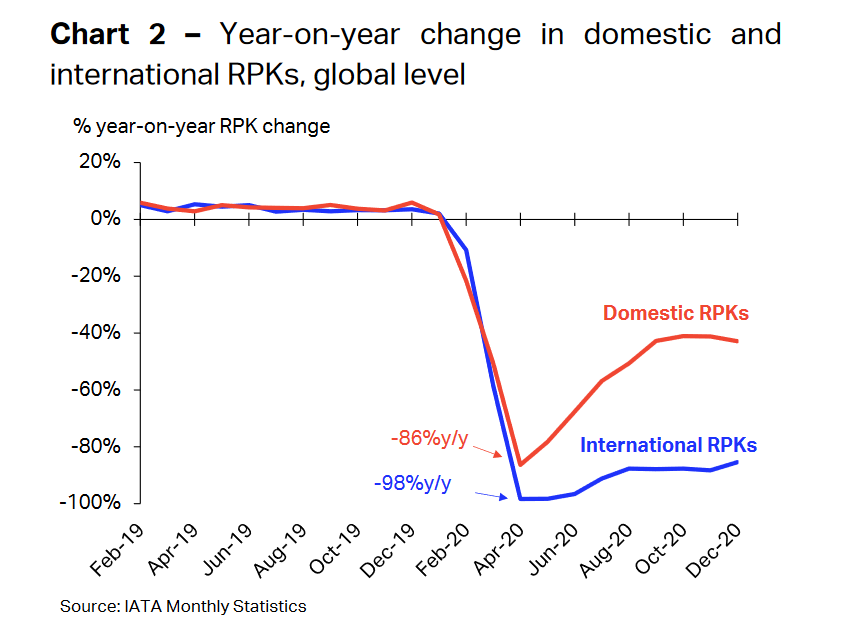

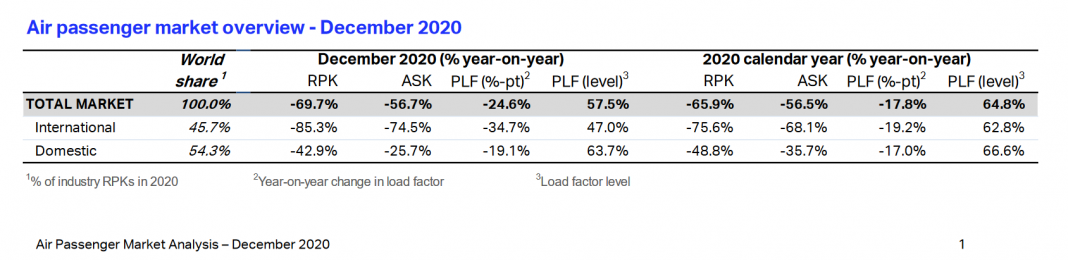

International passenger demand in 2020 was 75.6% below 2019 levels. Capacity, (measured in available seat kilometres or ASKs) declined 68.1%, and load factor fell 19.2 percentage points to 62.8%.

Domestic demand in 2020 was down 48.8% compared to 2019. Capacity contracted by 35.7% and load factor dropped 17 percentage points to 66.6%.

December 2020 total traffic was 69.7% below the same month in 2019, little improved from the 70.4% contraction in November. Capacity was down 56.7%, and load factor fell 24.6 percentage points to 57.5%.

Bookings for future travel made in January 2021 were down 70% compared to a year ago, putting further pressure on airline cash positions and potentially impacting the timing of the expected recovery.

IATA’s baseline forecast for 2021 is for a 50.4% improvement on 2020 demand that would bring the industry to 50.6% of 2019 levels. While this view remains unchanged, there is severe downside risk if more severe travel restrictions in response to new variants persist. Should such a scenario materialize, demand improvement could be limited to just 13% over 2020 levels, leaving the industry at 38% of 2019 levels.

“Last year was a catastrophe. There is no other way to describe it. What recovery there was over the Northern hemisphere summer season stalled in autumn and the situation turned dramatically worse over the year-end holiday season, as more severe travel restrictions were imposed in the face of new outbreaks and new strains of COVID-19.” said IATA’s director general and CEO Alexandre de Juniac.

| 2020 calendar year (% year-on-year) | World share1 | RPK | ASK | PLF (%-pt)2 | PLF (level)3 |

| Total Market | 100.0% | -65.9% | -56.5% | -17.8% | 64.8% |

| Africa | 1.9% | -68.8% | -61.0% | -14.4% | 57.4% |

| Asia Pacific | 38.6% | -61.9% | -53.9% | -14.3% | 67.5% |

| Europe | 23.6% | -69.9% | -62.1% | -17.4% | 67.8% |

| Latin America | 5.7% | -62.1% | -58.3% | -7.7% | 74.9% |

| Middle East | 7.4% | -72.2% | -63.3% | -18.5% | 57.6% |

| North America | 22.7% | -65.2% | -50.2% | -25.6% | 59.2% |

1% of industry RPKs in 2020 2Year-on-year change in load factor 3Load Factor Level